I know some people have been sitting on the sidelines all year…

Waiting for the right moment.

The right market.

The right price.

Well — this is it.

For Cyber Monday, you can get a full year of my Tim Sykes Letter and a 30-day trial of my AI forecasting tool, XGPT, for just $1.

That’s cheaper than a cup of coffee.

You’ll see the same kinds of setups I trade…

With AI-predicted prices down to the 1/1000th of a dollar.

If you’ve ever wanted to take trading seriously… this is your moment.

🎯 Start trading smarter for $1.

Let’s do this,

Tim

Medtronic Stock Finds Its Footing—Now It’s Gaining Momentum

Written by Thomas Hughes. Published 11/19/2025.

![]()

Key Points

- Medtronic's turnaround has taken time, but it is here and gaining momentum.

- Analysts and institutional trends indicate accumulation underway.

- Q2 results and the guidance update affirm strength and capital returns in F2026 and beyond.

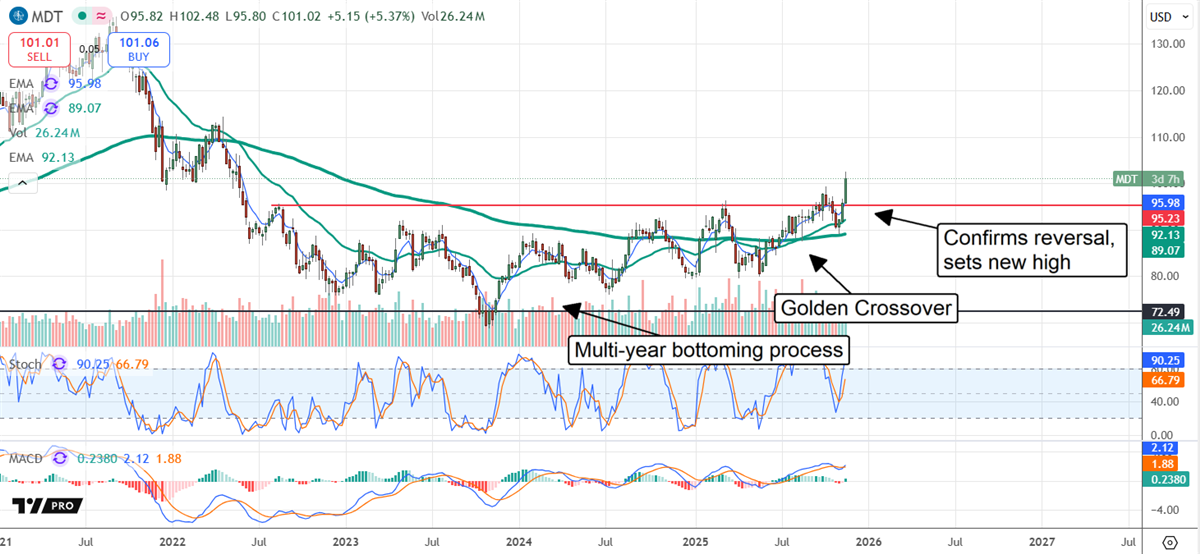

It took Medtronic (NYSE: MDT)

Chart action reflects that shift, indicating a bottoming process that unfolded over several years.

Who wants to buy dollars… for .18 cents?? (Ad)

A major shift is coming to the gold market — the world’s largest gold buyer is preparing to launch a new way for everyday Americans to invest in gold with a click, and when it goes live in 2026 it could unleash a wave of demand unlike anything we’ve seen. Garrett Goggin believes one $1.60 gold stock is positioned to be a prime beneficiary of this surge — a move where even a small price jump could mean a meaningful gain — along with several other miners set to ride the same trend.

Click here to see the $1.60 gold stock and Garrett’s full list of recommendationsKey details: price cleared a crucial hurdle in early 2025, formed a Golden Crossover, and confirmed a market reversal after the fiscal year 2026 (F2026) Q2 earnings release.

In this scenario, MDT could rally across the coming quarters—potentially for years—if it sustains modest growth, healthy margins, strong cash flow, and steady capital returns.

Medtronic’s stock could advance 20%–30%, possibly more, given the favorable growth outlook. The company is sustaining mid-single-digit growth in F2026, and results are accelerating, prompting guidance upgrades and suggesting consensus forecasts may be conservative.

As of mid-November, MarketBeat consensus forecasts expect mid-single-digit growth over the next five to six years, with gradual margin improvement along the way.

Capital returns are a significant factor — dividends, dividend growth, and share buybacks. The dividend yield of 2.95% is attractive; with a payout ratio around 50%, the payments appear sustainable.

Dividend increases are likely: the company is a Dividend Aristocrat with more than 40 years of consecutive increases, supported by earnings growth and a healthy balance sheet. Share buybacks continue to reduce the share count each quarter and are expected to be sustained for the foreseeable future.

Medtronic Fires on All Cylinders in Q2 F2026

Medtronic reported a strong FQ2, with growth across all segments and $8.96 billion in net revenue — a 6.6% year-over-year (YOY) increase and an acceleration from the prior year that slightly outpaced consensus.

Strength was underpinned by 5.5% organic growth and a 10.8% rise in the Cardiovascular portfolio, driven by a 71% jump in cardiac ablation sales. Diabetes sales climbed 10.3% year-over-year (YOY), with smaller gains in the Neurosciences and Medical-Surgical segments.

Margin news was positive. Operational execution and no tariff surprises drove incremental margin improvement and faster earnings growth. Adjusted earnings rose 8% versus a 6.6% revenue gain, outpacing MarketBeat consensus by a wider margin, and management expects the strength to continue.

Q2 strength prompted management to raise full-year guidance. The company increased its organic growth forecast by 50 basis points to 5.5%, slightly above consensus; the EPS-range midpoint now sits above consensus. Management may raise targets again after FQ3.

Institutional and Analyst Trends Indicate Accumulation Underway

Institutional and analyst trends indicate accumulation is underway. Institutions — which own more than 80% of shares — bought the stock steadily over the past 12 months and increased purchases in late Q3 and early Q4.

Institutional demand provides a supportive base, mirrored by analyst activity: expanded coverage, firmer sentiment, and rising price targets. The consensus price target of $103 implies modest upside, though recent updates suggest potentially larger gains.

The question now is whether these groups will continue to buy and lift targets; the Q2 updates suggest they will.

The post-release price action was solid. The stock jumped about 5% soon after the open, confirming support at a key pivot (the prior resistance and trading-range top) and setting a new high. That confirms a technical reversal and opens the door to a sustainable rally.